my comment: the article below is immoderate to say the least and I don't agree with a few things he says; however, there's a few nuggets of truth in there:

- tax loss selling is likely to produce even better buying opportunities in quality companies next month

- commodities could go down even further than they have and the recovery time will be difficult or impossible to predict, even if you believe that we are in the midst of a long term secular bull market in commodities

Tax-loss selling for 2008 will be the rule the next eight weeks.

Story By Rob Cornelius

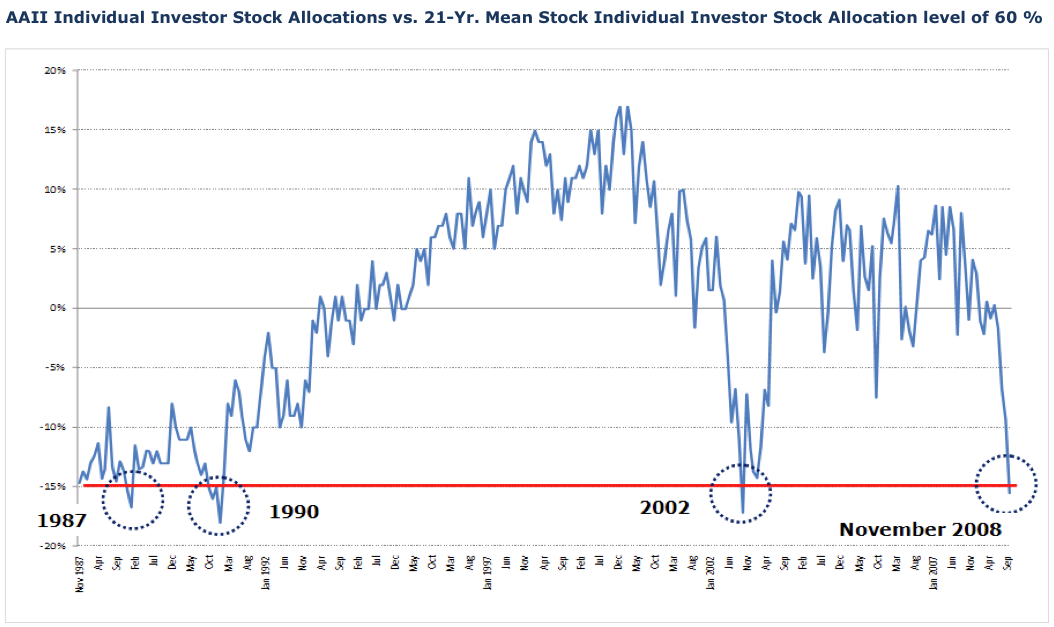

Money on the sidelines isn't coming back to the market. Don't expect the cavalry to show up and save us. Money that is out of the market either vaporized as losses, is in "safe" investments, such as U.S. government securities, or capitalizing one of these banks that is begging for deposits.

Preserving capital is critical. Nobody is feeling greedy yet.

Tax-loss selling for 2008 will be the rule the next eight weeks. Investors will sell their losers (and, boy, do we have a bunch of those) to make up for their gains. The pressure on stock prices should continue to be downward. Hedge-fund and mutual-fund redemptions will happen before year's end as well.

Carryover losses will be awesome. Investors have seemed to fear a Barack Obama presidency, and the last 1,500 points of Dow fall appear correlated to his rise in the polls. Some will sell to incur taxable losses; others who have huge assets are trying to get rid of them now to avoid changes in tax laws.

Retirement Plan DisastersPensions, charities and endowments will continue to hide behind terms like "unrecoverable losses." Read the daily newspapers and you see that term come up. That simply means losses they were forced to take by selling a devalued asset. There still are plenty more on the books that will have to be taken eventually. Understand that many of those organizations' stocks now need to go up 100 percent to be where they were a few months ago: If you are down 50 percent, you have to go up 100 percent to be even.

As S&P and Moody's do their jobs in coming months, more corporate bonds will be downgraded. More companies adjust earnings estimates down. When they drop below certain ratings thresholds, pension funds will be forced to sell them at market, cascading still further "unrecoverable" losses.

Pension funds were and are handicapped by being slow-moving, committee-driven animals -- late to bull markets and slow to evacuate bad ones. Not active, but reactive. And they are paying for it.

While state pensions have embarrassed all over the country, their corporate or private brethren may be worse; the former have the ability to raise shortfalls via taxes or bigger employee deductions. Ask U.S. Steel or the UMWA where their pension plans will be in a year. They are based on increasing share prices of the underlying company or adding more jobs/members. Neither is happening.

The Federal Pension Benefit Guarantee Corp. is seriously short of money, and a couple of good-sized corporate failures could deplete its kitty. It is like the FDIC for pension plans -- the insurance of last resort.

Someone will be made to take responsibility. In 2010 or 2012, this will be a political tool for un-electing state treasurers or anyone else vaguely responsible of either party.

The only upside of all this may be the fact that inflation, for the short term, is dead. Deflation is the word, as everything shrinks in value, be it homes or tons of coal or barrels of oil. But that said, I can never imagine a scenario when governments reverse cost-of-living-increases to those on the dole. They seem to have little self-interest in shrinkage.

People in many non-Roth IRAs and employee savings plans of all sorts are trapped. Some plans have no way to become un-invested other than money markets, which were shown to be potentially deadly in recent months. Worse still, you have no way to go short or bet against the markets. No sector has been safe for the last 90 days.

For those who are still mad at people who short stocks, it was pension funds that got rich as part of that process. To short a stock, some other investor must loan it to you. In most cases, it was big pensions, such as CALPERS loaning you those shares of Citibank and collecting margin interest on the loan. Like prostitution, it was a mutual agreement of two parties -- one of whom never really expected Citi to fall to $12.

Who Else Can We Blame?Illegal immigrants and their contributions to the real estate mess will be brought to the forefront to create scapegoats. National reporting states that as many as 5 million home mortgages may have been extended to illegal aliens, many of whom are in worse financial straits than Americans. In big, round numbers, and knowing that more illegals bought more homes in western states (where they are more expensive), say banks lose an average of $100,000 on each of those transactions. You're looking at a loss just there of $500 billion. Maybe that's overstating a dollar number, but protectionism and assessing blame tend to be big in economic disasters.

I cited "losers" and "poor people" as root causes of this crisis when I first started writing about it here on Aug. 9, 2007. That said, they were rational actors empowered by government to take what they knew they couldn't afford. When government told lenders to loosen standards so that anyone who could fog a mirror got a mortgage, these folks took advantage. Having everyone equal may be fine in a co-ed game of soccer among first-graders with no one keeping score. But in real life, some of you are richer/smarter/faster and get more playing time or score more goals. The market should reward that. Not all our children can be above average.

U.S. Dollar is StrongU.S. Bank government guarantees are bringing every dollar here to federally backed investments. This strengthens our dollar and weakens foreign markets' currencies. The eventual inflection point will be when the rest of the world loses faith in the Treasury to pay back and our rates to borrow suddenly skyrocket. That's when inflation should return. At this point, the best course of action may be to sell as much new debt as possible while rates are super low. As other nations cut interest rates to spur their own economies, the flight to U.S. dollars should intensify further.

Thank God the U.S. didn't make many loans to developing countries, whose currencies are crashing. Typical European banks may have those loans filling 20 percent of their books; the U.S. averages 4 percent. Crashing currencies make it harder to pay back your loans.

The idea of rising interest rates at the same time as deflation is pretty unique in economic history. No one is really sure how to model this crisis after anything else except maybe the American Panic of 1873.

Hard Assets SoftenCheap energy is a terrible sign for growth and the world economy.

Oil has more room to contract in price, as demand will slow further. The only thing keeping American refiners open is the fact that they can still make money on the middle distillates they refine (heating oil, diesel and aviation gasoline). They ship a lot of those to Europe. They are losing on auto gasolines right now. Once you see the diesel price in West Virginia slim down to maybe a 50-cent premium over regular gasoline, you'll know the refiners are in real trouble.

Low energy prices will destroy whatever progress has been made on alternative energy. Well-capitalized companies will do well as steel cheapens for massive windmills, but most of the solar guys were selling at ridiculous price/earnings multiples.

Ethanol is also dead if wholesale gasoline stays under $2 a gallon. Farmers may shift from corn to soybeans next spring for the sake of profits. Short term, alternative energy will expand only as a direct result of government handouts.

Gold/silver .... paper versus reality. Go to eBay. While gold that trades in the markets is less than $700, you see one-ounce gold coins selling for a three-digit premium to that at $850 or more. The percentage gap is still greater for silver and platinum.

People are hoarding gold and extra bullets it would seem. Central banks are trying to raise U.S. dollars and appear to be dumping physical gold while they can, depressing price. Price is now dropping enough to make mining unprofitable for not just gold but also many of the non-precious metals, such as copper and nickel.

Stop Whining, LearnGreat reads/blogs to scare yourself straight on this topic: calculatedrisk.blogspot.com, globaleconomicanalysis.blogspot.com, nakedcapitalism.blogspot.com ... and pay attention anytime "Dr. Doom" Nouriel Roubini or Oppenheimer analyst Meredith Whitney show up anywhere. Billionaire genius Mark Cuban at blogmaverick.com has been smart and full of good ideas, albeit with no sense of investment timing at all. All seem pretty sure our financial system isn't done with its turn in the spanking machine.

Rob Cornelius of Parkersburg follows energy and the markets for The State Journal.

![[Bill Miller]](http://s.wsj.net/public/resources/images/HC-GJ139_Miller_20061201204859.gif)