Value Investing vs. Value Pretending

For more than 50 years, great "value" investors — Warren Buffett, Benjamin Graham, Charlie Munger, Seth Klarman, to name a few — have been touting the benefits of investing when there is blood in the streets, buying businesses when they are on sale. At each turn, somebody would ask them: Aren't you concerned that, by constantly talking about how you became so successful, you'll create a following that will, in turn, increase competition and reduce your potential investment returns?

It is said that value investing is more popular today than ever before. I tend to disagree.

Investing ... 50 Years Ago

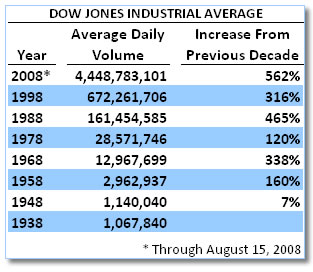

I am going to journey back to a time before I was born: 1958. The Dow Jones Industrial Average [DJIA] averaged about 10% a year from 1948 through 1957 (when looking at the average closing prices during that time). Stock prices were quoted in eighths and quarters, but most regular people only saw those quotes once a day — in the morning paper.

This was a time when you had to call a broker for a stock quote, who would in turn call a floor broker, who would then get the quote and update your broker. Assuming you didn't wait on the phone, your broker would call you back with a quote — sometimes several minutes later. Real time quotes and information? Not even a pipe dream yet.

It is said that Buffett never even had a tickertape machine in his office. And even if he did, how quickly could he really get price quotes? I mean — look at these things (right).

What chance did you have as a trader? Were you hand-plotting charts as they came across the tape? Then what? John Bollinger wouldn't be around to draw Bollinger Bands for another twenty-some years, Gerald Appel's MACD was still ten years away, and by the time you figured out your moving averages...they moved.

For the most part, regular people had absolutely no chance at being successful traders, speculators, or "growth" investors. To invest in stocks, you had one choice — buy stock in businesses that you would be comfortable holding for (i) at least an entire day, and (ii) regardless of the short-term swings.

There was no access to quick information; so, regular people had to buy knowing, and comfortable with the fact, that the price might be a few eighths or a few quarters higher or lower the next day. And when it was, you couldn't get too excited or too panicky because it took time for your broker to get an updated price — a price that could change rapidly in the few minutes it took for your broker to get the price, phone you back, take your order, and place and fill the order.

Investing Versus Speculating ... 50 Years Ago

Unless you were down on the floor of the exchanges every day, you had one of two choices: Buy great businesses when they were on sale (or down) or Buy random stocks, close your eyes, and hope for the best. In my dealings with people who had been saving and investing in the 1950s, I have found that most people opted for the first strategy. Even the most unsophisticated of investors invested soundly — buy great businesses, particularly when their prices were falling, and stay away from everything else.

What differentiated Warren Buffett from Aunt Bea and Grandpa Earl? One simple, yet often overlooked, thing: the breadth and scope of their respective Spheres of Confidence and Competence. Buffett was comfortable investing in a Sanborn Map — buying the business for less than the value of its stock and bond portfolio. Aunt Bea and Grandpa Earl didn't look for Sanborn Map; and, had they seen it, they didn't have the business and financial sophistication to buy and profit from it. Sanborn Map was outside their Sphere.

You know what else Aunt Bea and Grandpa Earl didn't do? They didn't see Buffett buying Sanborn Map and think, "Hey, we can do that too. Let's break up some businesses." Instead, they plodded along, buying stock in AT&T (T), Texaco, and other companies that seemed to have a big, sustainable presence in their area.

To Aunt Bea and Grandpa Earl, Sanborn Map was pure speculation. You know what? They were right! If they invested in Sanborn Map — without having Buffett's eye or ability — they would have been speculating. To them, speculating was uncomfortable and was to be avoided at all costs. After all, their goal was to invest so that they could one day be comfortable, and being uncomfortable throughout the process didn't make a whole lot of sense.

Along Came Wall Street

The 1950s began the Golden Age for Wall Street. Prior to that, brokers traveled the country, knocking on doors and selling stock. They would get checks from customers, finish their sales route, and then place the orders together — sometimes weeks after the customer first wrote the check. Remember: This was long before ACH, cell phones, and laptops. For crying out loud, Elvis Presley was just getting into the Army and it would be another year before Alaska would even become a state.

Technology. Advertising. Profits. By 1958, 83% of US homes had televisions — up from less than 1% in 1948, half of which were in or around New York City. And with television came...Wall Street commercials. It didn't happen overnight; but, eventually, the stock market became an exciting place where fortunes could be made...quickly.

The Schism on the Street

Aunt Bea and Grandpa Earl were not profit centers for Wall Street. They were boring, buy-and-hold investors — the type of clients a broker could go broke with. So, Wall Street had to "educate" them — teach them the difference between growth and value investing.

Sure, value investing is safe...but it's slow. Who wants 10% or 12% a year? These other stocks are ready to explode. They're gonna grow. They're...they're...they're growth stocks. Investing in growth stocks can get you to your goals two, no three, no...ten times faster.

Perhaps Aunt Bea and Grandpa Earl don't buy it. But their kids do. Born in the 1950s and 1960s, they started working and thinking about saving in the late 1970s and 1980s. Throughout the 1980s, young investors were growing more confused than their parents had ever been. On the one hand, the stock market was soaring and hostile takeovers, leveraged buyouts, and mega-mergers spawned a new class of billionaires. On the other hand, inflation and interest rates were out of control, banks were failing left and right, and the stock market was growing ever more volatile.

Aunt Bea and Grandpa Earl knew virtually nothing about the activities on Wall Street. All they knew was that Coca-Cola tasted great and everyone was talking about it.

The explosion in news, information, and selling the dream/showcasing the nightmare were the perfect recipe to create a new breed of investor: the short-term, growth-oriented trader.

"Old School" Investing Gets Murky

As "growth" and "value" became investment strategies, Wall Street built mutual funds and portfolio allocations around them. In time, "value investing" began to drift from its original meaning of "buying a sustainable business when it is on sale" to today's Wall Street definition of "investing in stocks that have low price to earnings ratios."

The Value Pretender

That fundamental shift in the definition of "value investing" leads us to Seth Klarman's Margin of Safety:

Value investing" is one of the most overused and inconsistently applied terms in the investment business. A broad range of strategies make use of value investing as a pseudonym. Many have little or nothing to do with the philosophy of investing originally espoused by Graham. The misuse of the value label accelerated in the mid-1980s in the wake of increasing publicity given to the long-term successes of true value investors such as Buffett at Berkshire Hathaway, Inc. (BRK.A, BRK.B), Michael Price and the late Max L. Heine at Mutual Series Fund, Inc., among others. Their results attracted a great many "value pretenders," investment chameleons who frequently change strategies in order to attract funds to manage.

These value pretenders are not true value investors, disciplined craftspeople who understand and accept the wisdom of the value approach. Rather they are charlatans who violate the conservative dictates of value investing, using inflated business valuations, overpaying for securities, and failing to achieve a margin of safety for their clients.

In short, Klarman is making the point that today's so-called value investments and value investors are, by and large, not true value investors in the old-fashioned sense of the word. To paraphrase Klarman: Value pretenders tend to buy what is down, without looking at whether or not it is cheap. They look at the PE ratio versus past PE ratios; they buy if the stock is trading near its 52-week low or wait until it pulls back from its 52-week high.

Investing...Today

Last month I wrote this post about business investing, and how it differs from "value investing" in the now traditional sense of the word. I guess I'm trying to start a revolution — a change in terms to help separate true value investors from value pretenders.

Answering the Question

Aren't you concerned that, by constantly talking about how [the gurus] became so successful, you'll create a following that will, in turn, increase competition and reduce your potential investment returns?

One thing that history has shown us is that most people are never really introduced to business investing, just growth and value investing/investments. And that makes a heck of a lot of sense. If you look at the expense ratio of the F Wall Street portfolio, you'll see that we effected just nine (now ten with the purchase of LNY) transactions in fourteen months. Any broker handling that account would starve to death having us as clients. Last year, four of the largest publicly held Wall Street firms generated more than $425 billion in revenue. To maintain that level of revenue on the backs of business investors, they would need more than 4.5 billion clients — roughly 70% of all individuals in the world.

But, if they can get you to double the number of transactions, they would need half as many clients to achieve the same level of revenue. If, on your own or (more likely) through their mutual funds, they could get you to do 100 transactions a year, they would need just 45 million clients — 99% fewer clients for the same revenue.

Thus, where is Wall Street's incentive to promote business investing?

The unintended result of these discussions about investing — growth investing, value investing/pretending, business investing — is that more people become interested, engaged, and intrigued. Sadly, many of these people don't have Aunt Bea and Grandpa Earl's patience and understanding (or the ability to recognize their lack of understanding) of investing, or the desire to learn how they should invest; so, they will jump from ship to ship in search of fast profits.

(Many people are so disgusted or disheartened with Wall Street and investing that they simply put it on the back burner, choosing to do nothing rather than risk making a mistake.)

This continued and growing trend will add more and more volatility which, in turn, can actually increase the potential for profits for true value investors but reduce the overall expected return for most "traditional" investors as they continue to trade and invest on emotion and lack of coherent, intelligent strategy.

Is value investing/pretending dead? It will have its moments in the sun. But mark my words: Business investing (Old-Fashioned Value Investing) will only get better.

(By the way: I don't have an Aunt Bea or Grandpa Earl. With a name like Ponzio? Think about it.)

No comments:

Post a Comment